In April 2026, the International Energy Agency (IEA) declared that the world has entered the Age of Electricity. The evidence came mostly from one source: solar energy.

Solar photovoltaic (PV) systems posted the largest annual electricity generation increase ever recorded for any energy source. It met more than 25% of all global energy demand growth in 2025, the first time a modern renewable source led that number. Solar now accounts for more than 8% of global electricity generation, generating over 2,700 TWh in 2025. That's more than double its 2022 output. Electricity demand itself grew at nearly twice the rate of overall energy demand, driven by EVs, data centers, and industrial electrification.

Solar has become the central technology for reaching net-zero emissions by 2050. The IEA's Net Zero Scenario requires roughly 7,000 TWh of annual solar generation by 2030. According to the IEA-PVPS Snapshot of Global PV Markets 2026, global cumulative capacity reached nearly 3 terawatts by the end of 2025, with over 600 GW added in 2025 alone. The annual installation rate has already passed what the IEA said we'd need by 2030. Grid integration and storage are now the binding constraints. While AI could solve the grid problem, portfolio company encosa is tackling the storage side of it for the German industry.

Policy support is mixed. The US Inflation Reduction Act triggered a manufacturing investment wave, but the residential solar tax credit ended at year-end 2025. The market kept moving anyway: in May 2026, solar overtook coal in the US electricity mix for the first time on record, supplying 12.8% of US electricity against coal's 12.2%, according to Ember. China set the pace globally, accounting for nearly 61% of all new solar capacity added in 2025.

Europe's picture is more stable. The EU hit its 400 GW installation target in 2025, backed by REPowerEU and a binding 42.5% renewable target by 2030. The 750 GW target for 2030 is now at risk, though. Installations contracted slightly in 2025, the first decline since 2016, driven by cuts to residential rooftop support across several member states.

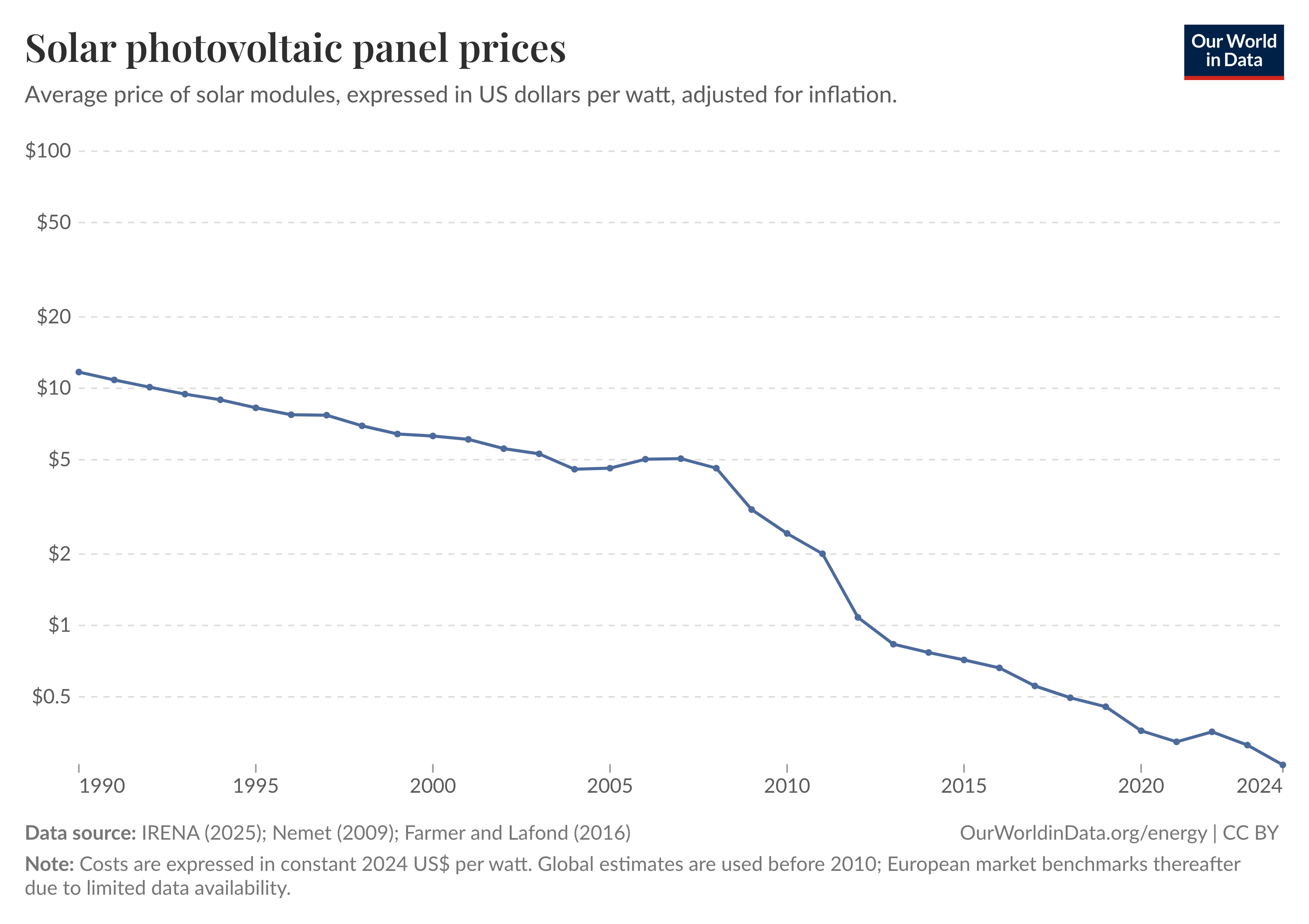

In the last 15 years, the price of solar panels has fallen from over $5 per Watt to below $0.50 per Watt at retail. At wholesale, BloombergNEF data puts module prices at approximately $0.096 per Watt in 2025, down more than 98% over two decades. According to REN21's Global Status Report 2025, Chinese factories produced roughly 630 GW of modules in 2024, nearly double China's own annual deployment, creating global oversupply that pushed prices down a further 45% year-on-year.

China remains the main reason solar costs keep falling. It's home to the top suppliers of solar manufacturing equipment, inverters, and battery storage. China accounts for roughly 80% of global solar PV manufacturing capacity across the entire value chain: polysilicon, wafers, cells, and modules. Additionally, in 2025, 88% of PV components imported into Germany originated from China.

China dominating all parts of the supply chain (see image below) is good on the one hand because it has pushed down prices through cheap (coal) energy, but on the other hand, it creates enormous dependencies in the long term.

Solar cells are the building blocks of solar panels. They are incredible creations that turn sunlight into electricity. To understand how they work, we need to examine their structure and the laws of physics that govern their operation.

The main parts of a solar cell are electrodes and semiconductor materials. The electrodes, usually made of silver and aluminum, help conduct electricity. The semiconductor material sits between the electrodes, with polycrystalline silicon being the most common, making up about 95% of the market. The choice of materials is important because it affects how well the solar cell works and how much it costs.

Today's solar panels transform only 20-25% of light into energy.

Solar cells turn sunlight into electricity. This starts when light particles, called photons, hit the silicon material. The electrons in the silicon absorb those photons, giving them extra energy and making them more mobile inside the silicon. By applying a voltage to the electrodes of the solar cell, an electric field is created across the silicon, and the mobile electrons start flowing and form an electric current. The sunlight has been converted to electricity.

Now, to add some quantum physics to the picture, electrons in semiconductors do not absorb continuous amounts of energy but rather specific packages of energy. If the energy of a package is too low, the electron will not absorb it; thus, a minimum of energy is needed. This threshold, called "band gap," is a very important material-specific property. In silicon, the band gap is 1.12 electronvolts (eV). That means the electrons in silicon can only absorb light that has at least an energy of 1.12 eV. Light below that threshold will not be absorbed.

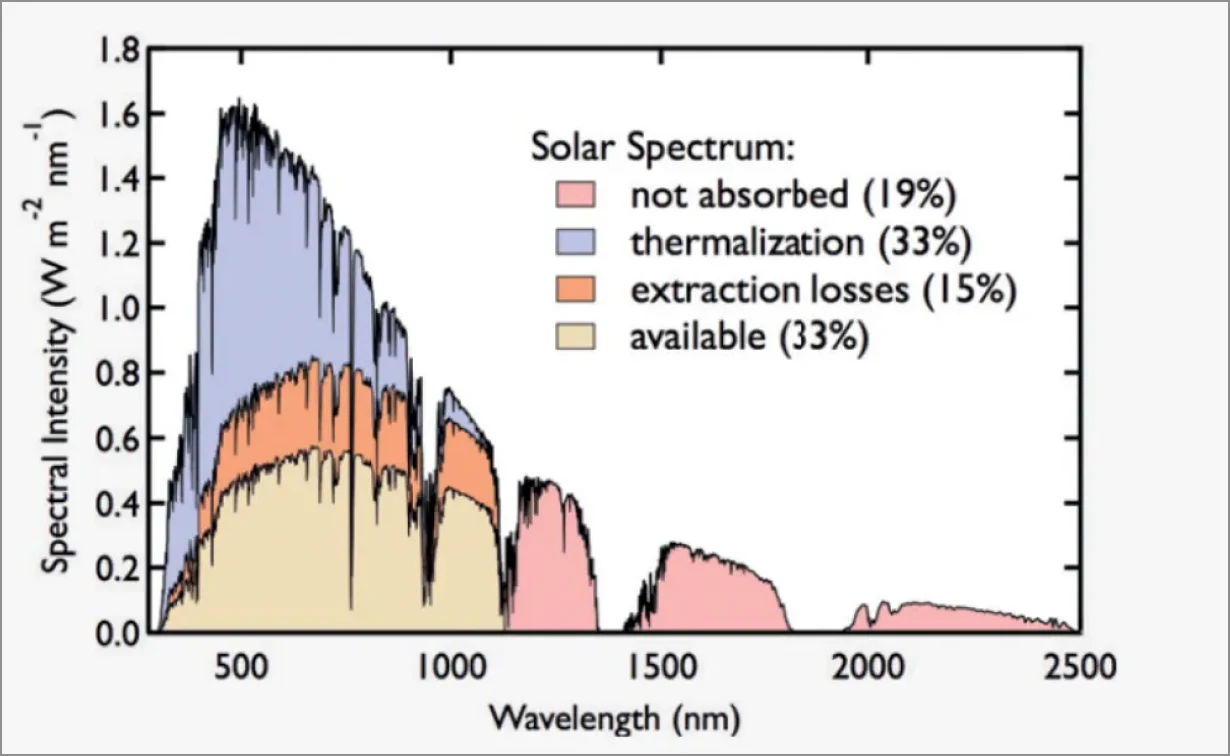

The energy of light is directly related to its frequency and, thus, its color. 1.12 eV translates to light with a wavelength of 1100 nanometers (nm) - this is infrared light. Visible light has a higher energy and a wavelength of 380 nm to 780 nm. Note that a smaller wavelength means higher energy. As a consequence, silicon solar cells can absorb some infrared and higher-energy visible light. But they cannot capture all of the light emitted by the sun. The image below shows the solar spectrum as measured on Earth and how much of that light is actually available for silicon solar cells. Light with a wavelength of 1100 nm - 2500 nm has an energy below the band gap threshold and is not absorbed. But too much energy is also not good as this extra energy is not always converted into more electricity, but instead lost as heat (thermalization). In the end, roughly 30% of the light remains to be transformed into electricity. This relates to the theoretical efficiency limit for simple silicon solar cells. The practical limit is even lower, at around 20%.

While this is not a bad number, there is room for improvement. Higher efficiency means more electricity, and people are trying different ways to make silicon solar cells more efficient. But most approaches just yield incremental improvements. Silicon offers many advantages in terms of cost and industrial handling, but it is far from being the best possible solar cell material. If we want to break through the efficiency barrier, we must explore materials beyond silicon.

Finding a better material than silicon for solar panels is critical to making them more efficient than standard cells' current 20% limit. A few options beyond silicon are being looked at:

One material that could replace silicon and become the semiconductor of future solar cells is Perovskite. This material class (there are different Perovskites available) offers several benefits:

The main challenge is durability. Silicon panels come with 25-year warranties and decades of field data. Perovskite cells degrade faster under moisture, oxygen, heat, and UV exposure, a problem that makes them not yet viable for standard utility-scale deployment, where project finance requires long warranties as a baseline. The industry is addressing this through better crystal structures, improved encapsulation, and more stable material compositions.

Perovskite materials also have a different band gap than silicon. They typically absorb the colors green (around 500 nm) and blue better (around 450 nm), while silicon is better in the red spectrum (up to 800 nm). Interestingly, the band gap of Perovskites can be tuned by changing the chemical composition of the material.

This "band gap flexibility" allows us to create a completely new and very exciting type of solar cell - so-called tandem cells. They share many advantages with Perovskite cells but add some new ones. They use two or more semiconductor materials that are good at absorbing different parts of sunlight due to slightly different band gaps. For example, Si-Perovskite tandem cells combine silicon with perovskite. This allows them to capture a wider range of light, making them more efficient. Optimized single-junction perovskite cells reach around 27% efficiency (NLR Best Research-Cell Efficiency Chart). Si-perovskite tandem cells have now crossed 34% in certified lab conditions. And since silicon is widely used in the solar industry, integrating perovskite layers with silicon cells can leverage existing manufacturing processes and infrastructure.

But it gets even more interesting once we combine different types of Perovskites. As discussed above, we can tune the band gap of Perovskite materials and then mix different Perovskites with different band gaps. This way, we could even achieve efficiencies of up to 50%. A quantum leap compared to current silicon cells.

Several companies are leading the way in making these advanced tandem solar cells:

OxfordPV is an Oxford University spin-off founded in 2010, backed by Equinor, Goldwind, and the European Investment Bank. Commercial shipments have begun from its Brandenburg, Germany facility. The current 'Centaur' module series delivers 25% module efficiency, with a 26% product planned for 2026. In April 2025, OxfordPV signed an exclusive patent licensing agreement with Trinasolar for the manufacture and sale of perovskite products in China. Current modules ship with a 10-year warranty. OxfordPV's public roadmap targets a 20-year lifetime by 2027 and 30 years by 2030, the threshold for full utility-scale bankability.

CubicPV, based in Bedford, Massachusetts, and backed by Breakthrough Energy Ventures, is pushing toward commercial scale. In July 2025, a collaboration with NREL produced a certified perovskite minimodule efficiency of 24.0%, the first time a US effort set a record in that category. Full-size pilot prototypes are in field testing. The 30%+ tandem module target remains the goal. Field testing of full-size prototypes is ongoing, but no commercial warranty has been published yet.

Caelux, a Caltech spinoff backed by Vinod Khosla and Reliance Industries, shipped its first commercial order in July 2025: Active Glass perovskite technology for a utility-scale project with a major developer. First real-world deployment of its approach. By adding perovskite as a coating on existing silicon panels rather than replacing them, Caelux also sidesteps some of the encapsulation challenges. The silicon substrate handles long-term structural durability.

The giant solar cell player First Solar in the US also invests in perovskite.

First Solar, founded in 1999, is the largest solar PV manufacturer in the Western Hemisphere, with $5.2 billion in revenue in 2025. It acquired Swedish perovskite startup Evolar in 2023, and in February 2026 licensed OxfordPV's patent portfolio for the US market. No commercial perovskite product has shipped yet. With roughly 18 GW of US manufacturing capacity targeted by 2027, its eventual entry into tandem cells would carry significant weight.

All these efforts show how fast and actively this field of solar technology is changing and growing. Perovskite and Tandem solar cells are increasingly recognized as the top contenders to surpass the performance limits of silicon while maintaining low costs. They could revolutionize the solar industry in terms of efficiency and applications, and bring solar cell production back to Europe. This would signify a paradigm shift in global solar technology manufacturing.

Oxford PV's production plant in Brandenburg is the clearest proof point for European solar manufacturing right now. The University of Stuttgart still runs strong perovskite research programs; Helmholtz-Zentrum Berlin and Fraunhofer ISE remain among the best labs in the world for this work.

Meyer Burger's collapse sharpens the challenge. Despite holding a genuine multi-year technology lead in heterojunction cells, the Swiss manufacturer couldn't survive the price pressure from Chinese production. Its German subsidiaries filed for insolvency in May 2025, with US operations following shortly after. The research partnerships with HZB, Fraunhofer ISE, and Stuttgart now lack a major European industrial partner to turn them into products.

So what does this mean for Europe? Europe can't compete with China on silicon. Meyer Burger tried and failed. But perovskite changes the equation in a few important ways.

First, the manufacturing process. Perovskite is processed at below 200°C, compared to above 1,400°C for silicon. That's a fraction of the energy input, which matters a lot in a continent with high electricity prices. Second, efficiency. Cells targeting 35%+ justify higher production costs through higher margins. You don't need to be the cheapest when your product is meaningfully better. Third, talent. Europe has some of the best perovskite research groups in the world. That's the input that matters here, not cheap coal.

The manufacturing case for European solar finally holds up. Getting there requires companies that can survive long enough to ship, which is the broader challenge we've been writing about for European industrial deep tech.